Digital banking is the delivery of banking services through digital channels, mainly internet browsers and mobile apps, without the need to visit a physical branch. It covers everything from checking your balance to applying for a loan, and in the case of digital-only banks, it’s the only way banking ever happens. As of 2026, more than 76% of bank customers worldwide use at least one digital channel for their transactions.

This guide covers how digital banking works, why it’s changing the financial industry, and what it means for you as a consumer or a professional in the fintech space.

What is Digital Banking?

Digital banking is the process of performing financial services and transactions through internet-connected devices instead of visiting a physical branch or using paper-based processes.

The term covers a wide range of activities:

- Checking your account balance on a mobile app

- Transferring money to another person in seconds

- Applying for a loan or credit card online

- Setting up automatic payments and savings

- Depositing a check by photographing it on your phone

Traditional banks offer digital banking as a supplement to their branch network. Digital-only banks, often called neobanks or challenger banks, operate exclusively through apps and websites. There is no branch to walk into.

What makes digital banking different from simply “using the internet to check your bank account” is the scope of it. Modern digital banking replaces nearly every banking interaction that once required a teller, a pen, or a counter.

A Brief History of Digital Banking

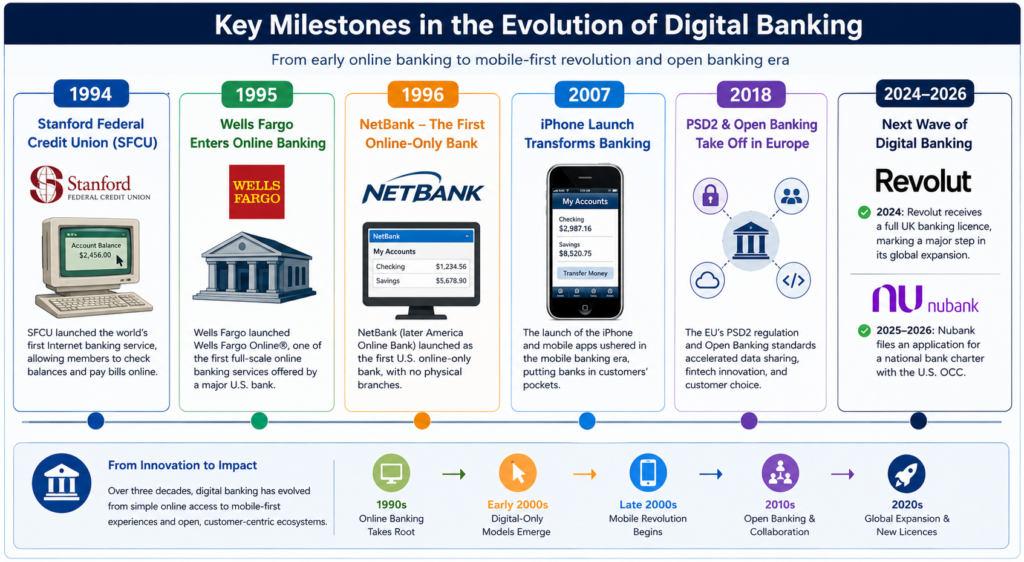

The story starts in October 1994, when Stanford Federal Credit Union became the first financial institution to offer internet banking to all of its members. It was basic by today’s standards: you could check balances and view transaction history online, and not much else.

Wells Fargo launched its own online banking service in 1995, becoming one of the first major retail banks to do so. By the late 1990s, the race was on. Banks spent heavily on internet portals, and purely online banks started appearing. NetBank launched in 1996 and ran as a branchless bank for over a decade before the 2008 financial crisis ended it.

The next real turning point was 2007. The iPhone arrived, and suddenly the concept of a touchscreen computer in your pocket capable of running banking software changed everything. Banks built mobile apps throughout 2008 to 2012, often hastily, and many of those early apps were frustrating to use. But the consumer behavior was cemented: people wanted to bank from their phones.

The third wave came with open banking. The European Union’s second Payment Services Directive (PSD2), which came into force in January 2018, required banks to open their data and infrastructure to licensed third-party developers through standardized programming interfaces. In the UK, the Competition and Markets Authority introduced its own Open Banking framework the same year. This moment, more than any other, enabled the neobanking explosion that followed.

Key Technologies Behind Digital Banking

Several technologies make modern digital banking possible. Understanding them helps explain why digital banks can operate with far lower costs than their traditional counterparts.

Application Programming Interfaces (APIs) APIs are the connective tissue of digital banking. They allow different software systems to talk to each other securely. When you connect a budgeting app to your bank account, an API is what makes that connection possible. Open Banking mandated standardized APIs, which let fintech companies build services on top of existing bank data.

Cloud Computing Traditional banks run on decades-old mainframe infrastructure that is expensive to maintain and slow to update. Digital banks are built on cloud platforms like Amazon Web Services, Microsoft Azure, or Google Cloud. This means they can scale rapidly, push updates instantly, and operate with much lower infrastructure overhead.

Mobile Technology Smartphones are the primary banking interface for most digital bank customers. Features like biometric authentication (fingerprint and face recognition), push notifications, and camera-based check deposit are all made possible by the hardware in modern phones.

Open Banking and PSD2 Open Banking transformed the regulatory environment in Europe and the UK. Under PSD2, banks must share customer data (with customer consent) and accept payments initiated by third parties through licensed providers. This created an entire ecosystem of fintech companies that could build products without needing to hold a banking license or build payment infrastructure from scratch.

Digital Banking vs Traditional Banking

This is the comparison that most people want to understand before making a decision about where to keep their money.

Traditional banks like JPMorgan Chase, HSBC, Barclays, or State Bank of India operate through a combination of physical branches, ATMs, and digital channels. They have been building their infrastructure for decades, sometimes longer. That history gives them scale, deep product catalogues, and trust built over generations. It also makes them slower and more expensive to operate.

Digital banks, by contrast, have no branches, minimal physical infrastructure, and technology built from the ground up for digital delivery. They move faster, charge less, and tend to offer a smoother user experience. Their weakness has historically been depth: fewer products, limited customer service options, and in some regions, questions about regulatory protection.

The honest picture is more nuanced than “old banks bad, new banks good.” What you prefer depends on what you actually need from banking.

| Factor | Traditional banks | Digital banks |

|---|---|---|

| Branch access | Extensive branch networks advantage | None or very limited |

| Mobile app quality | Variable, improving | Generally strong by design advantage |

| Account fees | Often higher monthly fees | Usually low or none advantage |

| Savings interest rates | Lower | Often higher advantage |

| Loan products | Full range — mortgages, auto, business advantage | Expanding, but limited at many |

| Customer support | In-branch, phone, chat advantage | Mostly chat and in-app |

| ATM access | Own ATMs plus network advantage | Partner ATM networks |

| Setup time | Days to weeks in some cases | Minutes in most cases advantage |

| Regulatory protection | Yes — FDIC, FCA, etc. | Yes, if properly licensed |

| International transactions | Often high fees | Usually lower fees advantage |

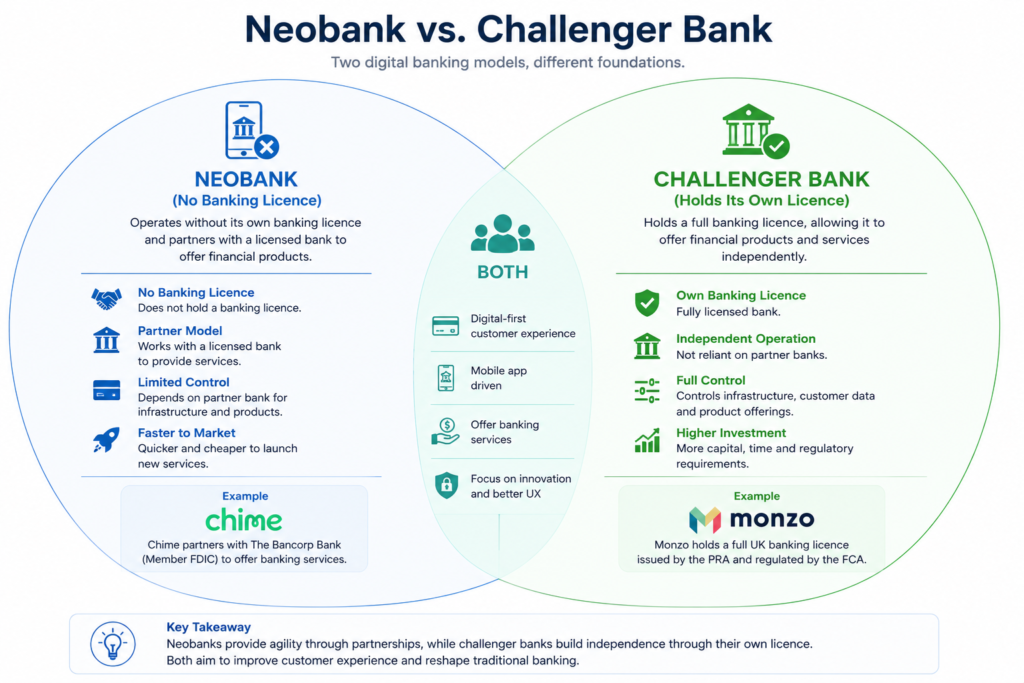

Neobanks and Challenger Banks Explained

The terms “neobank” and “challenger bank” are often used interchangeably, but there is a meaningful distinction.

A neobank is a financial technology company that offers banking-like services without holding its own banking license. Instead, it partners with a licensed bank to provide the regulated side of the service (deposit insurance, card issuance, payment processing). Chime in the United States works this way: its deposits sit at The Bancorp Bank and Stride Bank, both FDIC-insured. Chime provides the technology layer and the customer experience.

A challenger bank holds its own banking license and competes directly with established banks. Monzo and Starling Bank in the UK are challenger banks. They went through the full regulatory process to obtain banking authorizations from the Financial Conduct Authority, which means they can hold customer deposits directly and are covered by the Financial Services Compensation Scheme up to £85,000.

The lines between these two models are blurring fast. Several former neobanks are now pursuing banking licenses as they grow. Revolut received its long-awaited UK banking licence in 2024, and Nubank applied for a US OCC charter in October 2025. The direction of travel is clear: digital banks that start as technology companies eventually want to become fully licensed banks.

Popular Digital Banks Worth Knowing

The neobank space has grown significantly, with strong regional leaders and a few that are genuinely global.

Revolut (UK, founded 2015) Revolut is the largest neobank by valuation, now targeting a $75 billion figure in its latest capital raise. With over 70 million retail customers across 40+ countries, it has evolved from a fee-free foreign exchange card into a full-service financial platform offering stock trading, crypto, insurance, business accounts, and personal loans. In 2025, Revolut reported $2.2 billion in full-year revenue, up 31% year-over-year. In April 2026, it launched AIR, an in-app AI assistant, to its UK customer base.

Monzo (UK, founded 2015) Monzo serves over 12 million customers, representing roughly 22% of UK adults, making it one of the most adopted consumer apps in British financial history. Monzo turned profitable in 2024 and has built a reputation for strong budgeting tools, clear spending notifications, and a transparent product culture. It recently expanded personal credit and lending products as it works toward broader profitability.

Chime (USA, founded 2013) Chime is the largest US neobank with over 22 million customers. It built its market share by targeting Americans underserved by traditional banking: people who couldn’t afford monthly fees, those with thin credit histories, and workers who needed access to their paycheck a day or two before payday. Chime IPO’d in 2025, ending a long period of anticipation in the fintech community. Its SpotMe feature provides overdraft coverage up to $200 with no fees.

Nubank (Brazil, founded 2013) Nubank is the world’s largest neobank by customer count, with over 110 million customers across Brazil, Mexico, and Colombia. It went public on the New York Stock Exchange in 2021 and has since grown into the fifth-largest bank in Brazil by customer count. Nubank’s growth story is particularly notable because it expanded into a market where a large portion of the population had limited access to formal banking, and credit card interest rates at traditional banks were among the highest in the world.

N26 (Germany, founded 2013) N26 holds a full European banking licence and serves customers across the Eurozone. It was among the first digital banks to offer a genuinely pan-European banking product, though it pulled out of the US market in 2022 to focus on its core European markets. It has approximately 9 million active accounts.

Starling Bank (UK, founded 2014) Starling is notable for being one of the few neobanks that has been profitable for several years. Its founder, Anne Boden, built the bank with a particular focus on business accounts, and Starling has grown a strong small business banking product alongside its consumer offering.

Common Features of Digital Banks

The feature set across digital banks has grown considerably since the early days of instant notifications and foreign exchange cards. Here is what most established digital banks now offer.

Mobile App Features

The app is the branch. Everything you can do in a physical bank, a good digital banking app should let you do from your phone.

Account management View balances, recent transactions, and statements in real time. Set up and manage standing orders, direct debits, and scheduled transfers. Most apps update instantly when a transaction occurs, rather than showing a pending state for 24 hours.

Instant payments Send money to another person in seconds, whether they’re a contact in your phone or someone you’re paying for the first time. Peer-to-peer payment features like Monzo’s payment links or Chime’s Pay Friends work similarly to apps like Venmo but are built directly into the banking app.

Spending analytics and budgeting tools Digital banks automatically categorize your spending (groceries, transport, entertainment, dining out) and let you set budgets for each category. When you’re approaching your dining budget for the month, the app tells you. This feature alone has caused many customers to move their primary current account to a digital bank, because traditional banks rarely offer it with the same depth.

Mobile check deposit Particularly common in the US, where paper checks are still widely used. You photograph the front and back of a check, submit it through the app, and the funds typically appear within one to two business days.

Freeze and unfreeze your card instantly Lost your card but not sure if it’s actually gone? Every major digital bank lets you freeze your card in seconds through the app. You can unfreeze it just as quickly if it turns up under the sofa. This feature reduces unnecessary card replacements and the anxiety of waiting for a replacement to arrive.

Virtual cards Revolut and others let you generate a one-time or disposable virtual card number for online purchases. If that merchant gets hacked, your real card details are not compromised.

Savings pots and round-ups Create separate savings pots within the same account for specific goals (holiday, emergency fund, new laptop). Round-up features automatically round each purchase to the nearest pound or dollar and move the difference into savings. Small amounts add up noticeably over a year.

Account Types Available at Digital Banks

Digital banks now offer more than the basic checking and debit card combination they launched with.

Current/Checking accounts The core product. A digital current account typically comes with a debit card (usually Visa or Mastercard), account and sort code or routing number, and the full suite of app features.

Savings accounts Many digital banks now offer competitive interest rates on savings, often higher than what traditional banks pay, because their lower operating costs allow better rates. Monzo and Revolut both offer savings products with variable or fixed rates.

Credit products This area has grown considerably. Revolut, Monzo, Chime, and Nubank all now offer some form of personal credit, whether that’s an overdraft facility, a short-term personal loan, or a credit card. Nubank built much of its early growth on credit cards offered to people who previously had no access to them.

Business accounts Starling Bank, Revolut Business, and Monzo Business have become serious options for freelancers and small businesses. Low fees, fast onboarding (sometimes under 10 minutes), and strong invoicing integrations make them attractive compared to traditional business banking.

Joint accounts Monzo popularized joint accounts with a clear visual split of who spent what, which traditional banks rarely offer with that level of detail.

Benefits of Digital Banking

The growth of digital banking is driven by genuine advantages that customers experience daily, not just marketing.

Availability around the clock A traditional bank branch is open Monday to Friday, perhaps 9 am to 5 pm. Your digital bank works at 2 am on a Saturday when you realize you need to transfer money urgently. Customer support is available 24/7 through in-app chat in most cases.

Lower fees Traditional banks typically charge monthly account fees, international transaction fees, and ATM fees. Most digital banks offer free or low-cost accounts with no monthly maintenance charge and fee-free spending abroad on the base tier. Revolut, for instance, charges no foreign transaction fees on its standard plan.

Speed of onboarding Opening a bank account at a traditional branch can take days and require multiple documents in person. Digital banks have reduced this to a few minutes. You photograph your ID, take a selfie for identity verification, and your account is typically active within minutes. Some claim it takes less than five minutes from download to working card.

Real-time financial visibility Traditional banks often show a ledger balance that doesn’t account for pending transactions, and notifications can be delayed or non-existent. Digital banks push instant notifications for every transaction, show pending items clearly, and categorize spending automatically.

Better interest rates on savings Because digital banks operate with lower overhead (no branch network, fewer staff), they can pass some of that cost saving on in the form of higher interest rates on savings accounts. In the current rate environment, many digital banks are offering rates that beat the high street.

Financial inclusion This benefit is particularly significant in emerging markets. Nubank reached over 100 million customers partly because it offered credit cards to people who had been turned away by traditional banks. Chime built its US user base among the 20-25% of Americans who are underbanked, offering fee-free accounts with no minimum balance requirements.

Risks and Security in Digital Banking

Digital banking has real risks, and any honest discussion of the space has to address them directly. The good news is that the security architecture behind modern digital banking is substantial. The bad news is that the biggest threat comes from human behavior, not technology.

How Digital Banks Protect Your Money

256-bit SSL/TLS encryption All data transmitted between your device and the bank’s servers is encrypted using AES-256, the same standard used by government agencies. Intercepting that data without the encryption key is computationally infeasible.

Two-factor authentication (2FA) Most digital banks require a second form of verification beyond your password. This typically means a code sent to your phone, generated by an authenticator app, or confirmed via biometric (fingerprint or face recognition). Even if someone has your password, they can’t access your account without the second factor.

Behavioral analytics and fraud detection Digital banks run real-time machine learning models on your transaction data. If your card is suddenly used in three countries in one hour, or makes a purchase pattern that deviates sharply from your history, the system flags it immediately. Some banks will automatically block the transaction and send you an in-app alert to confirm whether it was you.

Instant card freezing As mentioned earlier, the ability to freeze your card instantly from the app is a security feature as much as a convenience. With a traditional bank, calling to report a suspicious transaction can take 20 minutes on hold.

Biometric authentication Most digital banking apps now support Face ID and fingerprint login, replacing passwords for day-to-day access. This is more secure than a password in most threat scenarios.

Deposit Protection

A common concern is whether money held in a digital bank is protected the same way it would be at a traditional bank.

United States: FDIC insurance covers deposits up to $250,000 per depositor, per institution. Chime’s deposits sit at FDIC-insured partner banks, so the coverage applies. SoFi holds its own bank charter and is directly FDIC-insured.

United Kingdom: The Financial Services Compensation Scheme (FSCS) covers deposits up to £85,000 per person at any authorized bank. Monzo, Starling, and Revolut (post-licensing) are all covered by the FSCS.

European Union: The EU deposit guarantee scheme covers up to €100,000 per depositor per credit institution.

The Real Risks

The honest security picture comes with some caveats.

Phishing and social engineering remain the top attack vector. No amount of bank-side encryption protects you if you hand your login credentials to a fraudulent website or share a one-time code with someone pretending to be your bank. Authorized push payment (APP) fraud, where people are tricked into sending money themselves, costs UK consumers hundreds of millions of pounds a year.

App-based account opening can be abused. The speed and ease of opening a digital bank account, which is a benefit for legitimate customers, is also attractive for identity fraud and money laundering. Digital banks have invested heavily in know-your-customer (KYC) and anti-money laundering (AML) systems, but the problem persists.

Customer support limitations. When something goes wrong with a traditional bank, you can walk into a branch. With a digital bank, you’re working through an in-app chat or a phone line that may have long wait times. For complex disputes, this can be frustrating.

Regulatory coverage varies by region. Not every country has robust deposit protection schemes, and some digital banks operating across borders are regulated in one jurisdiction while serving customers in others. Check what protection applies in your specific country before choosing a digital bank as your primary account.

How to Open a Digital Bank Account

The process is designed to be quick, but it does require a few things. Here is what the typical account opening looks like at most major digital banks.

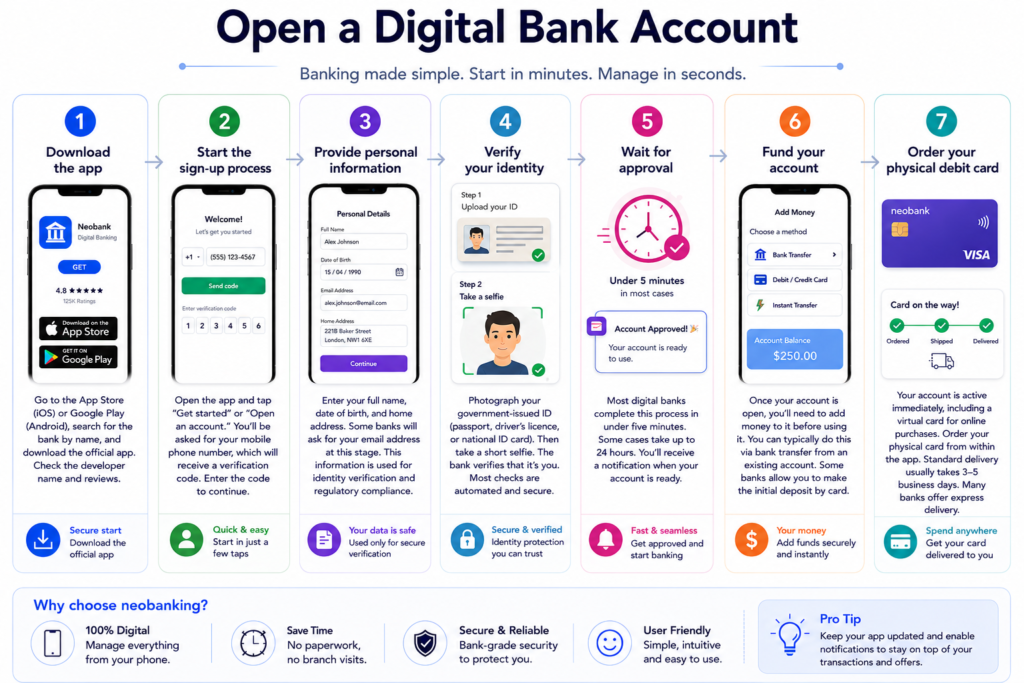

Step 1: Download the app Digital banks are app-first. Go to the App Store (iOS) or Google Play (Android), search for the bank by name, and download the official app. Check the developer name and review count before downloading to make sure you have the real app.

Step 2: Start the sign-up process Open the app and tap “Get started” or “Open an account.” You’ll be asked for your mobile phone number, which will receive a verification code. Enter the code to continue.

Step 3: Provide personal information Enter your full name, date of birth, and home address. Some banks will ask for your email address at this stage. This information is used for identity verification and regulatory compliance.

Step 4: Verify your identity This is the document verification step. You will be asked to photograph a government-issued ID (passport, driver’s licence, or national identity card depending on your country). After the document, you’ll typically take a short selfie video or a still selfie. The bank’s identity verification system compares the photo on the document to your selfie.

Most banks use automated systems for this step. Some cases are reviewed by a human analyst, particularly for complex documents or if the system has low confidence in the match.

Step 5: Wait for approval Most digital banks complete this process in under five minutes. Some cases take up to 24 hours, particularly if manual review is required. You’ll receive a notification when your account is ready.

Step 6: Fund your account Once your account is open, you’ll need to add money to it before using it. You can typically do this via bank transfer from an existing account. Some banks allow you to make the initial deposit by card.

Step 7: Order your physical debit card Your account is active immediately, including a virtual card number you can use for online purchases. Order your physical card from within the app. Standard delivery usually takes three to five business days. Many banks offer express delivery.

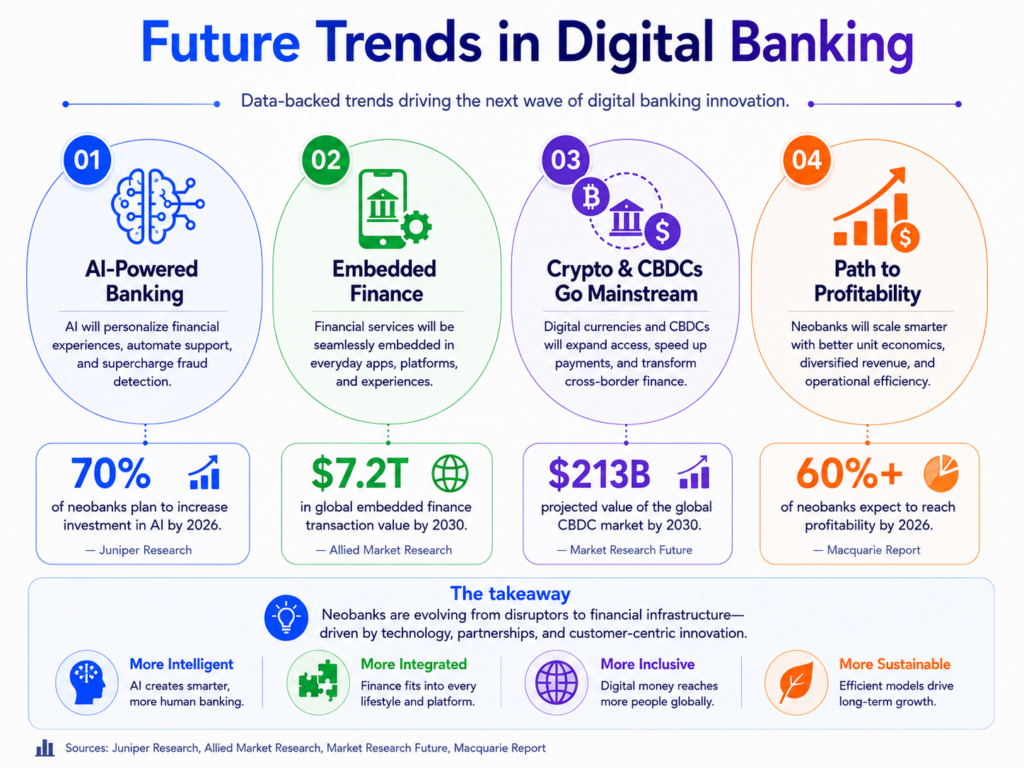

Future Trends in Digital Banking

The digital banking industry in 2026 is not a finished product. Several significant shifts are in progress that will change what banking looks like over the next five years.

AI-Powered Personal Finance

The integration of artificial intelligence into banking has moved beyond basic chatbots. Revolut’s AIR assistant, launched to 13 million UK users in April 2026, handles spending analysis, subscription management, card controls, and travel support through natural conversation. Monzo has invested heavily in machine learning for its lending and credit decisioning, as well as personalized spending insights across its 14 million customers.

The next generation of AI banking tools will go further. Proactive cash flow forecasting (telling you before you run low rather than after), real-time financial advice based on your spending patterns, and automated savings optimization are already in development at several major platforms.

Embedded Finance

Embedded finance refers to financial services being offered inside non-financial platforms. When you buy a laptop on an e-commerce site and the checkout offers you a buy-now-pay-later option, that’s embedded finance. When your ride-hailing app offers you insurance for the trip, that’s embedded finance.

Banking-as-a-Service (BaaS) infrastructure, provided by companies like Railsr, Synapse, and others, allows non-banks to add financial features to their products by connecting to licensed banking infrastructure through APIs. The end result is that your next bank account might come from a supermarket, a tech company, or a telecom provider rather than a bank.

Cryptocurrency and Digital Asset Integration

Revolut has offered crypto buying and selling since 2017. The question in 2026 is no longer whether digital banks will integrate crypto, but how deeply. The development of clearer regulatory frameworks in the EU (MiCA), the UK, and the US has opened the door to more comprehensive crypto banking products, including interest-bearing crypto savings accounts and instant crypto payments.

Central Bank Digital Currencies (CBDCs) are also moving from pilot to production in several countries. China’s digital yuan (e-CNY) has been tested with hundreds of millions of users. The European Central Bank’s digital euro project is progressing through development phases. When CBDCs arrive in mainstream use, digital banks will be the primary distribution channel.

The Profitability Challenge

One structural reality that the industry is still working through: 76% of neobanks remain unprofitable, earning an average of just $45 in annual revenue per user compared to $350 at traditional retail banks. The gap exists because most digital bank customers use them as secondary accounts, keeping savings and mortgages at their legacy bank.

The neobanks that have cracked profitability, primarily Revolut, Monzo, and Starling, have done so through subscription tiers, lending products, and business accounts. The industry trend is clearly toward depth: more products per customer, more reason to make the digital bank your primary financial relationship.

Branch Networks Under Pressure

The structural shift is visible in branch data. In the UK, over half of all bank branches have closed since 2015. In the US, more than 4,000 branches closed in 2025 alone. What remains is moving toward an advisory model: fewer transactional branches, more consultation centers for mortgages, financial planning, and business banking.

For most everyday banking needs, the branch has already become optional. The question for the next decade is whether it becomes irrelevant, or whether the human element of complex financial decisions keeps some physical presence alive.

Conclusion

Digital banking has gone from a novelty to the default for hundreds of millions of people globally. Over 76% of banking customers worldwide now use at least one digital channel for transactions, and 72% of payment transactions in developed economies run through digital interfaces.

The fundamental shift is not about apps replacing branches. It’s about financial services becoming genuinely on-demand, personalized, and accessible to people who were previously shut out by geography, fees, or paperwork. That trend has years of momentum behind it and no visible reason to slow down.

For consumers, the practical takeaway is straightforward: digital banking offers real advantages in cost, speed, and transparency for everyday financial management. The question is not whether to use it, but whether to use it as a supplement to your existing bank or make the switch entirely.

For financial professionals, the picture is a structural challenge to incumbent institutions that is still working itself out. The digital banks that achieve profitability at scale, building genuine primary banking relationships rather than secondary accounts, will define what the industry looks like in 2030.

The financial system is being rebuilt for a mobile-first world, and the rebuilding is well underway.

Frequently Asked Questions

Is digital banking safe?

Yes, with appropriate caveats. Reputable digital banks use strong encryption, two-factor authentication, biometric login, and real-time fraud detection systems that match or exceed what traditional banks deploy. Your deposits are protected by government schemes (FDIC in the US, FSCS in the UK, up to €100,000 in the EU) in the same way they would be at a high street bank, as long as the digital bank holds a proper banking licence or partners with one.

The main security risk is not the technology. It’s human error: clicking phishing links, sharing one-time codes with callers pretending to be the bank, or using weak passwords. Enable 2FA, never share verification codes over the phone, and you significantly reduce your exposure.

Do I need to visit a branch to open a digital bank account?

No. That is the fundamental design principle. Everything from account opening to loan applications happens through the app. Identity verification is done through document scanning and selfie comparison. Most accounts are fully operational within minutes of completing the application.

What happens if my digital bank shuts down?

If a properly licensed or FSCS-covered digital bank fails, your deposits are protected up to the applicable limit (£85,000 in the UK, $250,000 in the US per institution). The protection works the same as with a traditional bank. The key is checking whether your specific digital bank is covered in your country before depositing significant funds.

Can I get a mortgage or home loan from a digital bank?

This is changing rapidly. Revolut launched digital mortgage products in Lithuania, Ireland, and France in 2025, with more markets planned. Traditional comprehensive mortgage products remain more common at established banks and specialist mortgage lenders, but the gap is narrowing.

What is the difference between a neobank and a traditional bank?

A traditional bank operates physical branches, employs large staff, and runs technology built over decades. A neobank operates exclusively through digital channels, built with modern technology from the start, and typically charges lower fees. Traditional banks generally offer a wider range of products (mortgages, business loans, investment products). Neobanks typically offer a better user experience, faster service, and lower costs, particularly for everyday transactions.

Are the interest rates better at digital banks?

Savings rates at digital banks are often better than at traditional banks, because digital banks have lower operating costs and can pass some of that saving on to customers. This varies by market conditions and specific products. For checking or current accounts, the difference in interest earned is usually minimal, since most current accounts pay little or nothing.

What if I lose my phone?

Report the loss through another device by logging into the bank’s website or using a backup phone to access the app. Almost all digital banks let you remotely freeze your card and account immediately. You can also call the bank’s customer service line to report the loss. Once you have a new phone, you restore the app and re-authenticate with your credentials.

Can seniors or less tech-savvy people use digital banks?

Yes, though the experience varies. The best digital banking apps have been designed for ease of use and are accessible to people of all ages. Some users find the lack of a physical branch difficult, particularly for complex issues like disputing a large transaction or setting up power of attorney arrangements. If face-to-face banking matters to you, a hybrid approach (keeping a traditional bank account for complex needs while using a digital bank for daily spending) is a practical solution.

Is my money safer at a big traditional bank than at a digital bank?

Not necessarily, when it comes to regulatory protection. A £50,000 deposit at a licensed digital bank is covered by the FSCS to exactly the same extent as £50,000 at Barclays or NatWest. The risk profile is different in other ways: large traditional banks are considered systemically important and are unlikely to fail without government intervention. Some newer digital banks carry more uncertainty about their long-term viability. Established digital banks with years of operation, profitable accounts, and clear regulatory oversight are a different category from a startup that launched recently.

What is Open Banking and how does it affect me as a customer?

Open Banking, driven by PSD2 regulation in Europe and equivalent frameworks globally, means your bank is required to share your financial data with third-party providers if you give consent. In practice, this means you can connect your bank account to budgeting apps, accounting software, or comparison services without manually entering statements. It also means you can authorize payments directly from your bank account without giving the merchant your card details. Open Banking has made digital banking significantly more useful as an ecosystem.